PCAOB 2021 inspection reports: PwC sees best results again; EY deficiencies increase

By  Maria L. Murphy2022-12-22T17:40:00

Maria L. Murphy2022-12-22T17:40:00

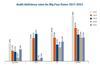

For the second straight year, PwC fared the best among inspection results released by the Public Company Accounting Oversight Board (PCAOB) for the largest U.S. audit firms, including each of the Big Four, Grant Thornton, and BDO.

The results, posted Monday, cover the 2021 inspection cycle. Only two of PwC’s 56 audits reviewed (3.6 percent) returned deficiencies, a slight increase over last year’s rate (1.9 percent) but still a far cry from the 30 percent the firm was at in 2019.

Second place among the Big Four firms went to Deloitte (13 percent), followed by EY (21.4 percent) and KPMG (25.9 percent). EY’s 2021 inspection results ended the firm’s prior trend of declining deficiencies in each year from 2017-20, while KPMG’s results improved for a fourth consecutive year.

THIS IS MEMBERS-ONLY CONTENT

You are not logged in and do not have access to members-only content.

If you are already a registered user or a member, SIGN IN now.

Related articles

-

Premium

PremiumPCAOB 2022 inspection reports: Big Four setbacks; KPMG redacted

Three of the Big Four audit firms saw increases to the deficiency rates observed in their latest Public Company Accounting Oversight Board inspection reports, while KPMG had its results redacted.

-

News Brief

News BriefPCAOB chair: Rising audit deficiency rates ‘completely unacceptable’

A steady increase in the rate of deficiencies observed by the Public Company Accounting Oversight Board during audit inspections the past three years has the head of the agency calling on firms to “make changes to turn things around.”

-

News Brief

News BriefPwC Australia removes chief risk officer after tax scandal review

PwC Australia exited eight partners, including its former chief risk and reputation officer, following an investigation into the sharing of confidential government tax policy information at the firm.

More from Accounting & Auditing

-

News Brief

News BriefEY compliance partner leaves after independence failings prompt regulatory investigation

Four senior partners at Big Four accountancy firm Ernst & Young, including a leader in the firm’s compliance function, have left the company because of spiralling repercussions from a costly compliance failure.

-

Premium

PremiumU.K. financial regulator looks to streamline audit enforcement procedures

Auditors are supposed to keep businesses honest, but how much regulation is the optimum for the auditors – and how onerous and punitive should the enforcement regime be? A new consultation by the U.K. regulator, the Financial Reporting Council, opened on Oct. 1 and has put the vexed question of ...

-

Article

ArticlePCAOB’s Christina Ho: How emerging technologies could improve audit quality

Emerging technologies, like artificial intelligence (AI) and advanced data analytics, can improve audit quality in significant ways. As the regulatory overseer of public-company audits, the Public Company Accounting Oversight Board (PCAOB) has a critical role to play by ensuring that its audit standards evolve as the audit profession evolves.